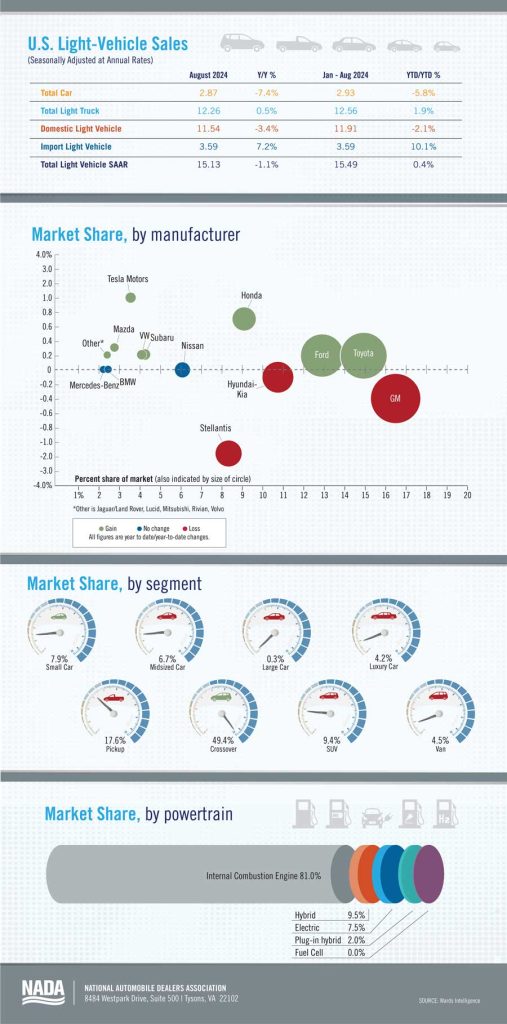

New light-vehicle sales in August totaled a SAAR of 15.1 million units, down 1.1% from August 2023’s 15.3 million. The August 2024 sales calendar included Labor Day weekend this year, which led to a raw sales volume totaling 1.42 million units, an increase of 7.6% year over year. Even so, after seasonal adjustment, August 2024’s SAAR was down slightly. Through the first eight months of the year, raw sales volume totaled 10.5 million units, up 2.2% compared with the same period last year.

As of July 2024, only the small-car and CUV segments posted year-over-year market share gains, with the biggest market share declines in the midsize and luxury car segments, which dropped 0.8 and 1.0 percentage points, respectively. Alternative-fuel vehicle sales increased in August. Sales of hybrids, plug-in hybrids (PHEVs) and battery electric vehicles (BEVs) together represented 19% of all new vehicles sold this year. Through the first eight months of 2024, hybrid sales were up 35.3%, PHEV sales rose by 17.8%, and BEV sales grew by 6.8% year over year.

New light-vehicle inventory has increased throughout 2024, and as vehicle inventory has risen so has OEM incentive spending. According to J.D. Power, average incentive spending per unit should total $3,035 in August, an increase of 59.5% from August 2023. J.D. Power expects the average new-vehicle transaction price this August to be $44,039, down 4.1% year over year. Average transaction prices have decreased because of higher OEM incentives and discounts.